The VA Overpayment Scam: Fake “You Owe the VA Money” Messages Are Hitting Veterans

Bottom line up front

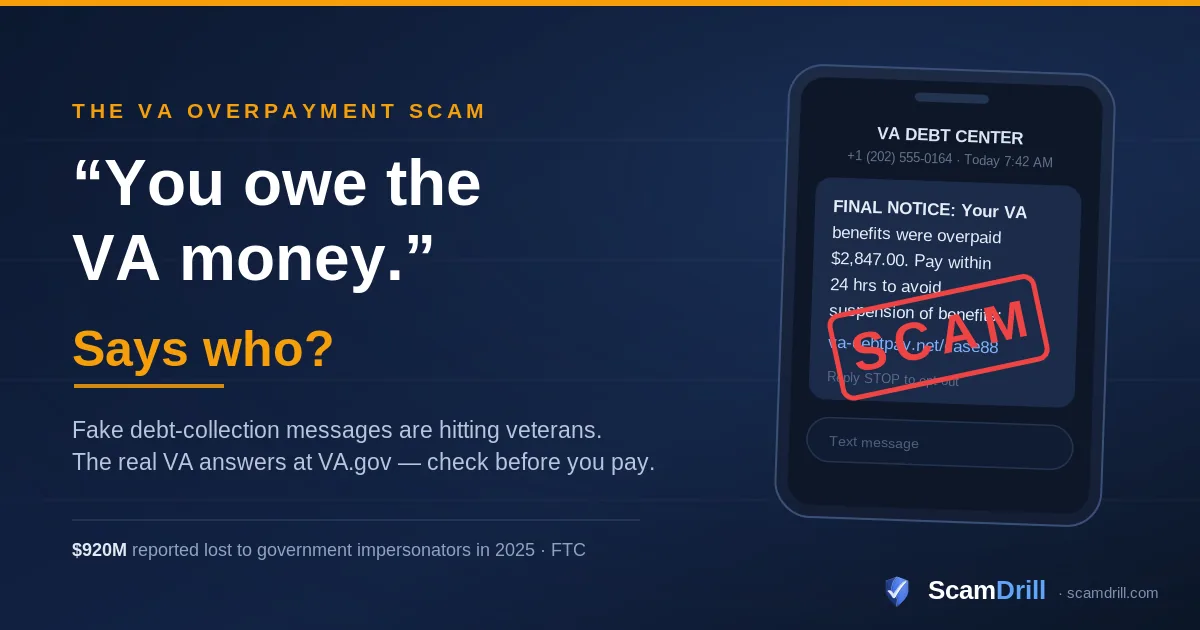

Scammers posing as VA staff are telling veterans, surviving spouses, and caregivers that their benefits were overpaid and the “debt” must be paid right now — by gift card, wire, crypto, or a link in a text. Real VA debt shows up when you log into VA.gov, and it gets resolved through the VA’s Debt Management Center at 800-827-0648 — with free repayment plans and waivers. Never pay or share information through a message that came to you. Check the source yourself first.

The reason this scam works is uncomfortable: the VA really does collect overpayments. Every year, ordinary benefit adjustments — a dependent who aged out, drill pay that overlapped with disability compensation, a pension recalculated after income changed — leave veterans owing money back, and the VA’s Debt Management Center sends real letters about it. Scammers don’t have to invent a believable story here. The VA already wrote it for them.

So when a call or text lands saying your benefits were overpaid and you need to settle up today, it doesn’t feel like an obvious con. It feels plausible. The FTC flagged the scheme for veterans and caregivers last summer, VA’s benefits office followed with a fraud alert of its own, and the warnings haven’t stopped since: June brought a fake “Veterans Savings Program” postcard, and the FTC opened July — Military Consumer Month — with a fresh advisory about debt-relief callers working the same crowd.

This guide covers what the fake messages look like, how to check whether you actually owe anything (it takes about two minutes), and what to do if money or information has already gone out the door.

Six signs a “VA debt” message is fake

Any one of these is enough to stop. You don’t need all six:

- It wants payment by gift card, wire transfer, crypto, or prepaid debit card. The VA never collects a debt that way. Nobody legitimate does.

- It pressures you to act immediately — pay today, or your benefits stop, or the debt “goes to enforcement.” Real VA debt notices give you time and options, not a countdown.

- The phone number or link isn’t VA.gov. Real overpayment debt is checked and resolved at VA.gov or through the Debt Management Center at 800-827-0648. A payment portal with a lookalike name is a trap.

- It asks for your VA.gov username or password. The VA will never ask for your login credentials. A scammer who gets them can do far worse than collect one fake debt.

- Someone wants a fee up front to “fix” or “reduce” your VA debt. Help with VA debt and claims is free — through the VA itself or an accredited representative. Charging before helping is the scam’s signature.

- The debt isn’t there when you log into VA.gov. This is the tiebreaker that settles everything else. If your account shows no debt, there is no debt.

Definition

VA overpayment scam: a government-impersonation fraud in which criminals pose as Department of Veterans Affairs staff and claim a veteran owes money for overpaid benefits. The demand arrives by text, call, email, letter, or postcard and pushes urgent payment through untraceable channels, or harvests VA.gov credentials and personal data.

Why this matters: a fake debt collector doesn’t need to fool you forever. They need about ten minutes of fear — long enough to walk you to a gift-card rack or a wire desk. The defense isn’t knowing every variant. It’s one habit: never resolve a debt through the message that told you about it.

Why this one lands on veterans

Government impersonation is the largest impersonation category the FTC tracks — people reported losing $3.5 billion to imposter scams in 2025 — and the VA version has three advantages the generic IRS or Social Security call never had.

First, the story is real. Overpayment debts are a routine part of the benefits system, common enough that the VA runs a dedicated call center for them. Many veterans have either had one or know someone who has. A scam that mimics a real, recurring piece of paperwork gets the benefit of the doubt a fake arrest warrant never earns. (Though people fall for those too — we took apart that con in our jury duty and arrest-warrant scam guide, and the skeleton is identical: a government voice, a debt, a clock.)

Second, the threat is aimed at the family budget. For a lot of households, the monthly VA payment is the floor everything else stands on. When a caller says that payment stops unless the “overpayment” is cleared, the fear isn’t abstract — it has a dollar figure and a due date, and unaddressed real VA debts genuinely can be recouped out of future checks. The scammer borrows that fact and weaponizes the urgency.

Third, veteran status isn’t a secret. Between data brokers, membership lists, and years of breaches, knowing who receives VA benefits — and roughly what kind — is cheap. That’s how the message arrives already sounding informed: your name, maybe your branch, sometimes a dollar amount precise to the cent. Precision reads as authority. It shouldn’t. It reads as a purchased mailing list.

The wider pattern of cons aimed at people who served — benefits buyouts, phony charities, records-for-a-fee sites — is its own topic, and we cataloged it in scams targeting veterans and the warning signs. The overpayment scheme is simply the entry on that list that’s surging right now.

The playbook, step by step

The contact. It might be a text with a payment link, a call from a number that displays as “Dept of Veterans Affairs,” an email with the seal in the header, or a letter dressed in convincing letterhead. VA’s fraud team says the fakes now copy official logos and formatting closely enough to be hard to tell apart on sight, and caller ID proves nothing — spoofing the displayed name and number is trivial, the same trick behind the fake USPS texts we broke down in our smishing guide.

The story. You were overpaid — a specific amount, often oddly precise. Maybe they blame a “system audit,” a dependency change, or a cost-of-living adjustment error. Precision and jargon do the persuading. Then comes the lever: repay now or your benefits get suspended, garnished, or referred for “federal collection action.”

The exit they offer. This is where it splits. Version one wants money: gift cards, a wire, crypto, a prepaid card, sometimes a “secure payment site” that exists to swallow card numbers. Version two wants access: they’ll “verify your identity” by asking for your VA.gov username and password, or a code texted to your phone. Version two is the one that should scare you more. A scammer inside your VA.gov account isn’t limited to one fake debt — they can try to reroute your direct deposit and take every payment after it.

The isolation. Like every con in this family, it ends with instructions not to verify: don’t call the main VA line, this case is handled only through this number; the call center “won’t have the file yet.” Any script that discourages you from checking with the source is telling you exactly what checking with the source would reveal.

What the VA will never do

- Demand payment by gift card, wire transfer, cryptocurrency, or prepaid debit card

- Ask for your VA.gov username, password, or a login code

- Threaten to suspend benefits unless you pay within hours through a link or a phone agent

- Charge a fee to help you manage or reduce a VA debt — that help is free

The variants making the rounds this summer

The overpayment demand has two active cousins, and it’s worth knowing both, because they hit the same mailboxes and phones.

The postcard that says you’re owed more

In June, VA warned about postcards promoting a “Veterans Savings Program” — extra benefits, CHAMPVA, TRICARE, dental coverage, supposedly available regardless of disability rating, if you call within five days. The card is bait. On the phone, the script runs on flattery about your service, then works toward your Social Security number and bank details. Same con as the overpayment demand, run in a mirror: one says you owe money, the other says money is owed to you. Both end at your identity.

The “military debt forgiveness” caller

The FTC’s July advisory describes cold-callers pitching enrollment in exclusive “military debt forgiveness” programs, often name-dropping USAA, Navy Federal, or a credit bureau to sound connected. The programs generally don’t exist. Two facts cut through every version of this pitch: it’s illegal for a debt-relief company to charge you before settling anything, and paying the caller instead of your real creditors torches your credit — which, for active-duty service members, can put a security clearance on the line. Real help is free: an on-base personal financial manager if you’re serving, VA financial counseling if you’re not.

How to check whether you actually owe the VA money

Here is the whole procedure, and it works for a letter, a call, a text, or a postcard:

- Close the message. Don’t call the number in it, don’t tap the link, don’t reply. If it’s a text and you want a second opinion first, paste it into our free SMS scam checker.

- Go to the source on your own. Type va.gov/manage-va-debt into your browser yourself and log in, or call the Debt Management Center at 800-827-0648 on a weekday. Your account shows current debts, amounts, and history.

- If a real debt is there, use the free options. The DMC offers monthly repayment plans, and you can request a waiver, a compromise, or a hardship pause — there’s a standard form (VA Form 5655) for exactly this. If you want help with claims paperwork, a VA-accredited representative costs nothing. Anyone charging an upfront fee to “handle” VA debt is running variant number three.

- If no debt is there, you’re done. The message was the fraud. Report it (details below) and move on with your day.

One more audience deserves a direct word: caregivers and adult children who manage a veteran’s mail and money. The FTC addressed its alert to you for a reason — these demands often reach the desk of whoever pays the bills, not the veteran personally. Put the DMC number (800-827-0648) in your contacts now, and treat any debt claim that arrives by phone or text as unverified until VA.gov says otherwise. If you’re already keeping an eye on an older parent’s accounts, our guide to reviewing a parent’s financial statements pairs well with this one.

If money or information already went out

No lecture here — this scheme is engineered by professionals who run it all day, every day. Speed matters more than blame.

- Cut contact. Stop answering, block the number, and don’t pay anything further — including any “reversal fee” they invent next.

- Call your bank or card issuer. Report the payment and ask what can be stopped, disputed, or flagged. If you bought gift cards, call the card company with the numbers; ask them to freeze whatever balance remains.

- Lock down your VA.gov account. If you shared a password or a login code, change the password immediately, turn on multi-factor authentication, and verify your direct-deposit details. If a payment ever goes missing, call VA at 800-827-1000 right away.

- Freeze your credit if your SSN went out. All three bureaus, free, takes minutes each. It blocks new accounts opened in your name.

- Report it. Your report is how the next veteran gets warned — and reporting quickly gives any investigation its best shot. Recovery is never guaranteed, but silence guarantees nothing happens.

Where to report

VSAFE (the government’s one-stop fraud line for veterans and military families): VSAFE.gov or 833-388-7233.

VA: 800-827-1000 if your benefits or VA.gov account may be affected.

FTC: ReportFraud.ftc.gov.

FBI: ic3.gov for texts, emails, and online payment trails.

Not sure what applies to your situation? Our “I’ve been scammed — what now?” tool builds the step list for you.

Talk about it — that’s the actual point of July

The FTC built Military Consumer Month around one finding: people who have heard a scam described before encountering it are far more likely to walk away. That’s a five-minute conversation at the VFW post, the family group chat, or the unit’s next safety brief. If your family has PCSed recently, fold in the rental-scam version of the same talk — moving season and benefits season overlap, and so do the people targeted by both.

Make “check VA.gov first” an automatic reflex.

ScamDrill sends your family realistic practice scenarios — including fake government debt demands — so the pause-and-verify habit is already there when a real one arrives. Setup takes under 10 minutes.

Start your family plan →The one line worth sending today

If there’s a veteran in your life — especially one who handles their own mail and doesn’t love asking for help — send them a single sentence: “If anyone ever says you owe the VA money, hang up and check VA.gov yourself, or call 800-827-0648. If it’s real, the VA gives you free ways to fix it. If it’s not there, it was a scam.”

Thirty seconds to send. And it plants the exact reflex this scheme is built to outrun.