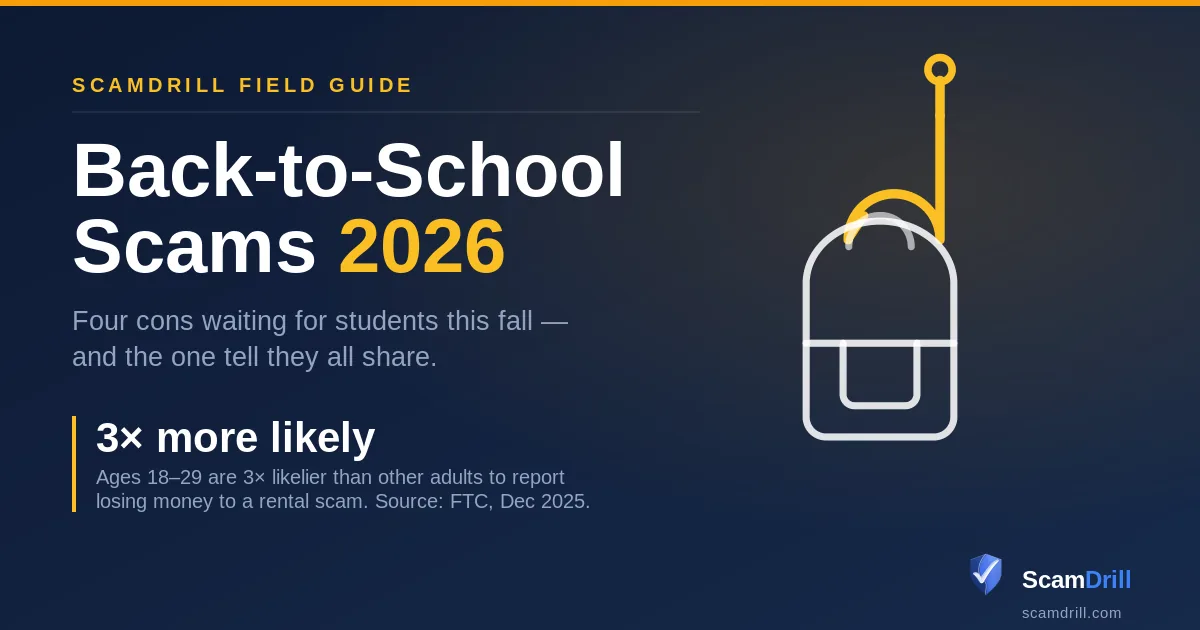

Back-to-School Scams 2026: The Four Cons Waiting for Students This Fall

Bottom line up front

Four cons cluster around move-in season: the fake scholarship, the fake loan-forgiveness program, the phantom apartment, and the fake school or storefront. They share one tell — money or a credential has to leave you before anything real arrives. Federal aid, scholarships, and forgiveness programs are free to apply for; a fee is not a hurdle on the way to the money, it is the money. And students are getting hit disproportionately: the FTC finds people aged 18 to 29 are three times more likely than other adults to report losing money to a rental scam.

The back-to-school window is the one stretch of the year when a nineteen-year-old is expected to move real money. Deposits, tuition balances, textbooks, a first apartment, a laptop, aid paperwork. All of it happens in about six weeks, most of it online, much of it for the first time, and nearly all of it against a deadline someone else set.

Scammers know the calendar. They are not improvising in August — they are running the same four plays they ran last August, with better graphics.

What follows is each play, what it looks like from the inside, and the single question that kills it.

Seven signals that a back-to-school offer is a scam

Every con in this piece trips at least one of these. Most trip three.

- There is a fee attached to free money. Scholarships, grants, FAFSA, and federal forgiveness programs cost nothing to apply for or receive. An “application fee” or “disbursement fee” is the entire business model.

- It found you. Real scholarship committees do not slide into DMs. Real servicers do not cold-call about a program closing tonight.

- Someone wants your FSA ID. That credential is a legal signature. No school employee, consultant, or “aid specialist” has any business holding it.

- No human will meet you at the apartment. The landlord is traveling, the agent is unavailable, and here is a lockbox code instead.

- The price is wrong in your favor. Rent far under the market near campus. A $340 textbook for $22. Bargains are the bait, not the product.

- The payment channel has no rewind. Zelle, Cash App, Venmo, wire, gift cards, crypto. Chosen precisely because the money does not come back.

- The clock belongs to someone else. “Three spots left.” “The portal closes at midnight.” Manufactured urgency is what stops you from checking.

Definition

Back-to-school scam: fraud timed to enrollment and move-in season, when students and families make unusual payments under deadline pressure. The common forms are fake scholarships, phony loan-forgiveness programs, fraudulent rental listings, and counterfeit school or textbook sites. Each one either charges a fee for something free or harvests credentials to steal aid money.

Why students get hit harder than anyone

There is a stubborn myth that fraud is a problem for the elderly. It is a problem for the elderly. It is also, in raw frequency, a young person’s problem, and the housing data makes that unmissable.

In its December 2025 analysis of rental fraud, the FTC found that people aged 18 to 29 were three times more likely than other adults to report losing money to a rental scam, and that 46% of all rental-scam loss reports came from that age band alone. The agency specifically noted that many young adults were targeted inside the Facebook groups students use to hunt for sublets near campus (FTC Data Spotlight, December 2025).

The reason is not that students are gullible. It is that students are doing high-stakes financial transactions in exactly the venue scammers own. In 2025, nearly 30% of people who reported losing money to any scam said it started on social media, with reported losses hitting $2.1 billion — about eight times the 2020 figure of $261 million (FTC Data Spotlight, April 2026). Among 18-to-29-year-olds who reported a loss, 40% said the scam began on a social platform — the highest share of any age group.

Apartment hunting on Facebook. Textbook deals from an Instagram ad. A scholarship posted on TikTok. A campus job in a group chat. That is the whole freshman supply chain, and it runs through the channel with the worst fraud numbers in the country.

Source: ScamDrill analysis of FTC, FCC and U.S. Department of Education fraud guidance, 2025–2026.

Con 1: The scholarship that charges you to win it

The pitch is flattering and specific. You have been selected. The award is real money — $2,500, $5,000, sometimes more. There is one small administrative step: a $25 processing fee, or a $35 verification charge, payable now to lock the award.

The fee is small on purpose. It is calibrated to sit below the threshold where a person stops and calls someone. Twenty-five dollars is not worth a phone call to your parents. That is precisely why it is twenty-five dollars.

The variants are worth knowing because they don’t all look like this:

- The advance-fee award. You “won” something you never entered. Pay to unlock it.

- The paid scholarship database. Legal, mostly useless. The listings are free through your financial aid office and through the Department of Education. Paying does not improve your odds; it just moves money.

- The application harvest. No fee at all. The “application” just wants your Social Security number, your date of birth, and your bank details for “direct deposit of the award.” That is not a scholarship form. That is an identity-theft intake form.

The question that ends it

“What is the fee for?” A legitimate scholarship has no answer, because a scholarship is money moving toward you. Any sentence that ends with you sending money is the wrong direction.

Con 2: “Loan forgiveness” that forgives nothing

Federal repayment and forgiveness programs are real. Access to them is free, always, through StudentAid.gov and your loan servicer. Nobody can move you to the front of a line that has no line.

The scam sells the paperwork. A company — often with a name engineered to sound governmental — offers to “enroll” you in a special program, for a fee. Sometimes they want an ongoing monthly “servicing” charge. Sometimes they want you to redirect your loan payments to them. Always, at some point, they want your FSA ID so they can “handle it for you.”

Hand that over and you have handed over a legal signature. With an FSA ID, someone can change your contact details, change your school, and change where your aid disbursement lands. The Department of Education’s Federal Student Aid office is blunt about it: nobody but the account holder should ever have it.

Charging an advance fee for federal student-loan debt relief is also, separately, illegal under the FTC’s rules. That is a useful fact but a poor defense — the companies doing it are not deterred by rules, and by the time enforcement lands, the fee is gone. The defense is refusing to pay in the first place.

Free is the whole point

Income-driven repayment, consolidation, deferment, forbearance, PSLF certification — every one of these is a free form you can file yourself. If someone charges for it, they are charging you for the privilege of doing something you could have done in an afternoon.

Con 3: The apartment that was never for rent

This is the one that empties a bank account, and it is the one aimed most precisely at students.

Here is the mechanism, straight from the FTC’s report. Scammers copy a real listing — frequently a property that is actually for sale, not for rent — swap the contact details, cut the price, and repost it somewhere else. About half of rental-scam reports in the year ending June 2025 said the scam started with a fake ad on Facebook. Another 16% pointed to Craigslist.

Then they solve the obvious problem: how do you convince someone a place is real without showing it to them? Two answers, and both are clever.

The first is the lockbox trick. They copy listings from landlords who use self-guided-tour services, then send you a code to open the lockbox holding the keys. You let yourself in. You walk the unit. It feels completely legitimate, because it is a real apartment — just not theirs. (The FTC notes that scam warnings posted inside some of these homes have tipped people off, which tells you how common this has become.)

The second is the credit-check affiliate scam. They ask you to prove you’re creditworthy and send a link to a site offering a credit check for a dollar. That dollar quietly enrolls you in a recurring paid membership, and the scammer collects an affiliate commission on every sign-up. Sometimes that is the entire scam — they never even wanted the deposit.

And the third pattern is the plainest one: an application that asks for your Social Security number, a photo of your driver’s license, and your paystubs, before you have agreed to rent anything. That is identity theft wearing a landlord’s coat. Legitimate landlords pull your credit themselves. They do not ask you to fetch it for them.

Source: FTC Consumer Sentinel Data Spotlight, “Rental scams hit home with $65 million in reported losses,” December 2025.

The three checks that take four minutes

- Search the street address by itself. If it shows up at a different price, with a different contact, or listed for sale — it’s a copy.

- Compare the rent to the block, not to your budget. Meaningfully cheap near campus in August is not luck.

- Refuse to pay before a person, in person. A lockbox code is not a person. A video tour is not a person.

Con 4: The school that doesn’t exist — and the storefront that doesn’t ship

This one is newer, and it is the clearest example of what generative AI changed about fraud.

In December 2025, the Department of Education launched a public page on fake schools, warning that scammers are standing up convincing college websites built with AI-generated content, staged videos, and chatbots — institutions that claim to offer real degrees and real financial aid, sometimes under names deliberately close to those of legitimate schools (U.S. Department of Education, December 11, 2025). Students apply. Students pay fees. Students hand over the personal data needed to file aid applications in their name.

The scale of the aid-fraud problem behind it is not small. The Department says it has blocked more than $1 billion in attempted federal student-aid fraud since January 2025, after discovering that roughly $90 million had been fraudulently disbursed — including more than $30 million paid out on applications tied to deceased individuals and more than $40 million to companies running bots dressed up as students. When it switched on identity verification in June 2025, it flagged nearly 150,000 suspect identities in FAFSA forms in the first week.

That fraud has a victim who is rarely mentioned: the real person whose identity was used. We wrote about that specific harm in ghost-student FAFSA fraud — where the first sign that your identity was used to claim federal aid is a bill, a tax notice, or a loan in your name for a school you have never attended.

The retail cousin of the fake school is the fake storefront. Shopping fraud is the single most-reported scam type that starts on social media, and the FTC’s 2025 data shows the most common outcome is the simplest one: people paid, and nothing ever arrived. Textbooks at a fraction of list, a MacBook at half price, a dorm-furniture bundle from a brand you have never heard of — the ad is targeted at you using the same audience tools a real business would use, because scammers buy ads too.

How to check a school or a seller in 60 seconds

- Type the school’s exact name into the Department of Education’s official databases — not the search box on the school’s own site.

- Read the URL character by character. Fake sites lean on near-miss spellings of real institutions.

- For any seller: search the company name plus “scam.” Then pay by credit card, which gives you chargeback rights that Zelle and Cash App do not.

The FSA ID is the master key. Treat it like one.

If you take one operational habit from this piece, take this one.

The FSA ID is not a login. It is a legal signature on federal documents. It can move where your aid money goes. Parents share it with kids, kids share it with parents, roommates “help” each other file, and a shocking number of people give it to someone who called claiming to be from their school’s aid office.

Rules that hold up:

- Nobody gets it. Not a consultant, not a “debt relief specialist,” not someone who called you.

- Two-factor authentication on, always. And never read a verification code aloud to anyone — that code is the last wall, and asking for it is the oldest move in the playbook.

- If it is compromised: change the password, then call the Federal Student Aid Information Center at 1-800-433-3243, then report to the Department of Education’s Inspector General at oig.ed.gov/oig-hotline and to the FTC at IdentityTheft.gov.

What to do in the first 60 minutes after you pay a scammer

Speed is the only leverage you have, and it decays fast. In order:

- Call the money first, not the police. Your bank, your card issuer, or the payment app. Ask for a reversal or a recall by name. Zelle and Cash App are hard, not always impossible — but only if you call immediately.

- Screenshot everything before it disappears. The listing, the profile, the chat, the payment confirmation. Scam accounts get deleted within hours.

- Lock the credential, if one was exposed. Change the FSA ID password, change any reused password, turn on 2FA.

- Freeze your credit at all three bureaus if you handed over an SSN or a photo ID. It is free, and it takes about ten minutes.

- Report it. ReportFraud.ftc.gov, the platform where the ad ran, and — for rentals — the local police in the city where the property sits, because some universities and landlords will act on a report number.

- Tell your school. The financial aid office has seen this before, and if the con is circulating on campus you have just warned the next student.

Then brace for the second wave. Within days or weeks, someone will contact you offering to recover the money you lost, for a fee. It is not a coincidence and it is not a good samaritan; victim lists are a product. We took that con apart in The Second Scam. And if you want a step-by-step plan rather than a checklist, what to do after a scam walks through the whole sequence.

Reading this helps. Rehearsing it works.

ScamDrill sends your family realistic practice scams — the fake scholarship email, the too-good rental text, the “verify your FSA ID” page — so the tells fire automatically when a real one lands in August. Setup takes under 10 minutes.

Start your family plan →Why a warning wears off and a drill doesn’t

Here is the uncomfortable part. Your student can read this entire article, agree with all of it, and still wire a deposit three weeks from now.

Not because they forgot. Because the scam does not arrive in a calm moment. It arrives at 11pm the night before the housing deadline, when four other apartments have already gone, when the “landlord” is friendly and reassuring and has an answer for every question, and when saying no feels like losing the last place near campus. Urgency does not defeat knowledge by argument. It defeats knowledge by exhaustion.

What survives that moment is a reflex — a small, automatic stall that buys ten minutes. We wrote about the machinery behind it in how scammers persuade you, and the same pressure levers show up in the campus-adjacent cons we covered in micro-task and fake-job scams aimed at young adults and QR-code scams aimed at teens. If you have a younger sibling heading into high school rather than college, the groundwork starts earlier — that’s the tween and teen internet safety guide.

If a message lands and you cannot tell, our free SMS scam checker and email scam checker will give you a read in a few seconds, and the how-to-spot-scams reference is worth a bookmark before move-in.

The one message to send before move-in

If you have a student in your life, send them this, verbatim, today:

“Before you send money to anyone this fall — a landlord, a scholarship, a loan company, a seller — text me the link first. I’m not checking up on you. Everyone gets fooled by the good ones, and the good ones show up when you’re out of time. Two minutes on my end costs nothing.”

The point of that message is not the check. The point is giving a nineteen-year-old, standing in front of a deadline, permission to stall. That permission is worth more than every red flag on this page.