The “Pay Yourself” Scam: When Your Bank’s Fraud Department Isn’t Your Bank

Bottom line up front

A text that looks like a fraud alert from your bank. Then a call from the “fraud department.” Then instructions to reverse a bogus charge by sending money to yourself on Zelle. There is no charge, the agent is the thief, and the money you “send yourself” lands in their account. No bank will ever ask you to move money — to yourself or anyone else — or to read out a security code. Hang up and call the number on your card.

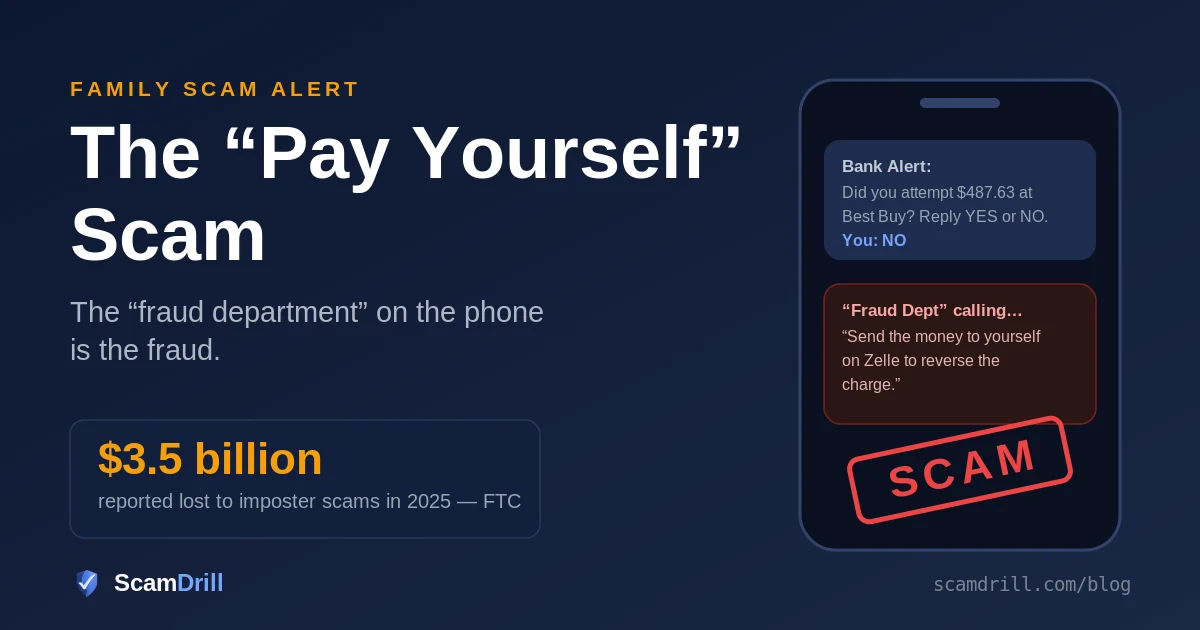

It starts with a text that looks exactly right: “FreeMsg: Did you attempt a charge of $487.63 at Best Buy, Columbus OH? Reply YES or NO.” You didn’t, so you reply NO — which is precisely what your bank would tell you to do with a real alert.

About a minute later, your phone rings. Caller ID shows your bank’s name. The agent is calm and professional, gives you a case number, and reassures you: the charge was flagged, no money has left yet, and they can reverse it right now. There’s hold music. There’s call-center murmur in the background. Nothing about it feels like a scam, because everything about it was built not to.

Then comes the one sentence the entire production exists to deliver: “To pull the funds back, you’ll just send the money to yourself with Zelle — same phone number, same account, it never leaves your name.”

It does leave your name. That’s the whole trick, and it’s working at scale: the FTC counted more than a million imposter-scam reports in 2025, with losses up nearly 20% to $3.5 billion — the ninth straight year imposters topped the fraud charts. This guide breaks down how the callback con works, what the “send money to yourself” request actually does, and the two-step exit that beats every version of it.

Five tells, any one of which ends the call

You don’t need to out-argue a professional. You need one of these, then a dial tone:

- Anyone asks you to send money to yourself. Zelle’s own network says it plainly: your bank will never ask you to send money to yourself — not to reverse fraud, not to “verify” the account, not for any reason.

- Anyone asks you to read back a one-time code. The code is not a formality. The code is the theft — more on that below.

- There’s a countdown. “We can only reverse the charge in the next 30 minutes” is pressure dressed up as helpfulness. Real fraud cases don’t expire while you think.

- You’re told to ignore your bank’s own warnings. If the app throws up a “is this a scam?” screen and the agent says “that doesn’t apply to reversals,” the agent is asking you to overrule the bank on the bank’s behalf. Sit with that one.

- The caller wants credentials after “verifying” you. A real fraud team already has your account. It will never need your password, PIN, or login code — the FTC lists that request as a defining mark of the fake fraud-activity call.

Definition

Pay yourself scam: a bank-impersonation fraud in which a fake fraud-department agent, following a fake fraud-alert text, persuades you to “reverse” a bogus charge by sending money to your own phone number or email through Zelle or a similar app. A one-time code trick reroutes the transfer to the scammer’s account.

Why this call gets past smart people

Most scam scripts ask you to do something for a stranger. This one asks you to do something for yourself, against a stranger. That inversion disarms the exact instinct that protects you everywhere else.

Think about what the victim believes is happening at each moment. A thief tried to steal from them. Their bank caught it. A professional is now helping them claw it back. Every action they take — replying NO, answering the call, opening Zelle — feels like defense. The scam doesn’t recruit your greed or your loneliness; it recruits your vigilance. People who’d never wire money to a prince will absolutely “secure their own account,” fast, while a reassuring voice reads them a case number.

The set dressing carries the rest. Caller ID spoofing makes the phone say the bank’s real name — the same cheap trick behind the fake USPS delivery texts that flooded phones the last two years. The opening text mimics real fraud-alert formats down to the merchant-and-amount phrasing. Some crews even open with “we will never ask for your PIN or password” — borrowing the bank’s own security language as a credibility prop before asking for something worse. It’s the authority playbook we broke down in our guide to how scammers persuade you, running at phone-call speed.

What the “security code” actually does

The mechanical heart of the scam is boring, which is why nobody explains it on the call.

When you enroll a phone number or email with Zelle, the network verifies you own it by texting a one-time code. Punch in the code, and that phone number becomes an address that points at your bank account. Money sent to the number lands in the account it’s linked to.

The scammer’s move: while they have you on the phone, they start enrolling your phone number on their bank account. Zelle dutifully texts you a verification code. The “agent” asks you to read it back — “to authorize the reversal” — and the moment you do, the enrollment completes. Your number no longer points home. It points at an account the crew controls, often opened with stolen credentials and burned within days.

Now “send money to yourself” means exactly what it says on their side of the table. You type your own phone number as the recipient, you see your own name or number on the confirmation screen, and the network routes the money to the account that number now belongs to. Zelle’s own explainer spells out both halves of the defense: your bank will never ask for that code, and it will never ask you to pay yourself.

Why this matters beyond one scam: the one-time code is the master key to most of your financial life, and every crew on the phone knows it. Whatever the story — reversals, refunds, “account verification,” a delivery that needs rescheduling — the request to read back a code is the same request. Decline it everywhere.

The same con in other costumes

The Venmo and Cash App version

Swap the bank for the app and the script survives intact. A text says your Venmo account is compromised; the callback walks you through “verifying” with a sign-in code, upgrading to a “business account” to unlock protection, or moving your balance to a “secure” address. Cash App gets the same treatment, sometimes with fake support numbers seeded into search results so victims dial the scammer directly. The rule doesn’t change: no payment app calls you to ask for codes or transfers, and no legitimate support line is reached by calling a number from a text message.

The “safe account” escalation

The pay-yourself trick empties what’s in checking. The patient version goes after everything else. The FBI calls it the Phantom Hacker: a tech-support impersonator “finds” hackers on your computer, hands you to a fake bank fraud department, which hands you to a fake government official, each layer pushing the same instruction — move your savings somewhere “safe” while they catch the intruder. In the first half of 2023 alone, IC3 logged 19,000 tech-support-scam complaints with more than $542 million in estimated losses; nearly half the victims were over 60, and they carried 66% of the damage.

That version is aimed squarely at retirement money, and it’s growing: FTC analysis found reports of older adults losing $10,000 or more to this move-your-money con more than quadrupled between 2020 and 2024 — and combined reported losses above $100,000 jumped eight-fold, from $55 million to $445 million. The FTC’s counter-rule is absolute, and worth quoting because it has no exceptions to remember: never move your money to “protect it.” Your money is fine where it is. Anyone who says otherwise on an unexpected call is the reason it wouldn’t be.

And when a bank blocks the suspicious transfer — as banks increasingly do — the crews improvise around the block. Some now send a “courier” to the victim’s door to collect cash directly, a variant ugly enough that we gave it its own guide last week. Same skeleton throughout: a trusted institution, a manufactured emergency, and your money leaving through a door the institution supposedly opened. It’s the identical frame as the jury-duty arrest-warrant call — only the badge changes.

What your bank will never do on a call or text

- Ask you to send money to yourself, or to anyone, to “reverse” or “secure” anything

- Ask you to read back a one-time code, password, or PIN

- Tell you to move funds to a “safe” or “protected” account — that account is the scam

- Rush you past the warnings inside its own app

The two-step exit

Everything above compresses into a habit that takes ten seconds and defeats every variant at once:

- Hang up. Not politely, not after one more question. The person on the line is either a scammer or a real bank employee who will completely understand. There is no third option, and neither one is harmed by a dial tone.

- Call the number on your card. Flip your debit or credit card over and dial what’s printed there, or use the phone number inside your banking app. If the fraud case is real, it’s attached to your account and any agent can see it. If it isn’t there — and it won’t be — you just kept your money by doing nothing.

The callback step matters more than people expect. Scammers don’t fear skepticism on the call — they’re trained for it, and arguing with them is their home turf. They fear the hang-up, because no script survives you independently dialing the real institution. Suspicious texts deserve the same detour: before you reply to any “fraud alert,” you can paste it into our free SMS scam checker for a read on the red flags.

One more habit worth building into your household: if you help a parent with their finances, tell them about this scam before the phone rings — people warned about a script in advance are far more likely to hang up on it. Our guide to protecting elderly parents from scams covers how to have that conversation without condescension, and the Phantom Hacker numbers above are the reason to have it this month rather than eventually.

If money already moved

The people who fall for this are not careless. They’re usually the ones who responded fastest to what looked like a threat against their own account. If that’s you or someone you love, move now and sort feelings later:

- Call your bank immediately — the number on your card. Say the words “I was scammed” and ask them to attempt a stop or recall on the transfer, freeze Zelle enrollment on your profile, and re-secure online banking. Minutes matter for recalls.

- Un-enroll and re-enroll your Zelle address. If the scammer captured your number via the code trick, your phone number may still point at their account. Your bank can reset the enrollment so future payments to your number reach you again.

- Change your online banking password and add the strongest login protection offered. If you shared any credentials, assume they’ve been tried elsewhere too.

- Ask about reimbursement — without counting on it. Truly unauthorized transfers carry strong federal protections. Transfers you were deceived into approving are harder, but since 2023 Zelle’s network rules have required participating banks to review qualifying imposter-scam claims. Report fast, be precise about the impersonation, and get the claim in writing.

- File the reports. ReportFraud.ftc.gov and ic3.gov. Reports are how patterns get traced and how the next family gets warned.

Two follow-ups people skip

Watch for the second scam. Victim lists get resold, and “recovery agents” who promise to claw your money back for a fee are the next con in line.

Not sure what applies to you? Our “I’ve been scammed — what now?” tool builds a step-by-step plan for your exact situation, and our family recovery guide covers the longer road.

Make the hang-up reflex automatic — before the real call comes.

ScamDrill sends your family realistic practice scenarios, including fake bank fraud alerts, so the pause-verify-call-back habit exists before a professional tests it. Setup takes under 10 minutes.

Start your family plan →The one sentence to send your group chat

Most people have never heard of this scam until the phone is already ringing, and the whole scheme dies on contact with one line of advance warning. Send this to the family thread today: “If ‘the bank’ ever calls about fraud and asks you to send money to yourself or read back a code — hang up and call the number on your card. Banks never ask for either.”

Ten seconds to send. It costs the scammer their entire production budget.